Mutual Funds vs Index Funds: What You're Actually Paying

Overview of mutual funds

Using a mutual fund offers a great deal of convenience, but their fees are generally very high (1 to 3%). If you’re still holding bank mutual funds, the fee math in this article is why switching to index ETFs pays off over decades. There are two types of mutual funds:

Actively managed: These pay fund managers large sums to buy and sell stocks frequently in hopes of “beating the market.” This also increases your fees substantially because you need to pay for the manager’s salary plus the cost of transactions and other investment drag. There is no evidence that any major institution’s mutual funds have beaten the market for any extended period of time.

Passive mutual funds: These are generally on the cheaper side of mutual funds as they don’t have many of the fees actively managed funds do, but even a 1% drag will cost you hundreds of thousands in the long run, and it’s super easy to cut that fee to 0.15 to 0.3%.

Ben Felix has a great video on this if you want to watch:

Run your actual holdings through the Portfolio Fee Audit to see the dollar cost of your blended MER over 10, 20, and 30 years.

How to compare mutual funds to index funds

The stock market returns have been crazy since COVID, which makes looking at mutual funds very appealing: most mutual funds have grown 10 to 20% in the last year so 2% feels relatively small. Furthermore it’s really hard to compare the returns of mutual funds to indexes because their asset allocations can change (a balanced mutual fund may shift from 60% bonds to 40% and still be considered balanced), which will increase their return and make it seem like the mutual fund is beating the market when they really just increased your risk exposure.

For the sake of comparison I pay 0.145% in fees on my VEQT index portfolio. Here is a visualization of my portfolio approximately.

Trying to compare the returns of a specific mutual fund to a specific index fund is never going to be an apples-to-apples comparison. Rather, if we can agree that there is no evidence that mutual funds beat a comparable index fund over the long term, we can instead focus on the asset allocations and pick an index fund that matches your risk profile.

TL;DR: While a mutual fund may beat an index for 1 to 5 years, we know it will underperform on average. Don’t look at the returns of a mutual fund. Look at the allocation. Once you’ve matched your risk profile to an all-in-one ETF, VEQT vs XEQT is the most common fork in the road—and either choice beats staying in mutual funds.

Anatomy of an index fund

Allocation, allocation, allocation! It’s all about the allocation. You’re likely aware of stocks (sometimes referred to as “equity”) and bonds (also called “fixed income”).

Equity is the portion of your portfolio that provides the most growth. Over the last ~100 years the expected return on a diversified equity portfolio over any 30-year period is about 10% annually.

Bonds or fixed income provide stability to your portfolio. Over the long term bonds have provided returns of 3 to 5%, though this has been much lower since the 1990s because of increasingly cheap interest rates globally.

The rates above don’t include inflation (~2 to 3% annually), which reduces the “buying power” return for equities to ~8% annually and 1 to 3% annually for bonds.

I know there are a lot of links and terms, but it’s really simple to find an index that works for you because most indexes with the same risk profile will perform similarly. Check out What are all-in-one index funds for a rundown of popular options.

How to pick your index fund

Pro-tip: Every mutual fund should have a “prospectus” available online where you can see exactly what you’re invested in.

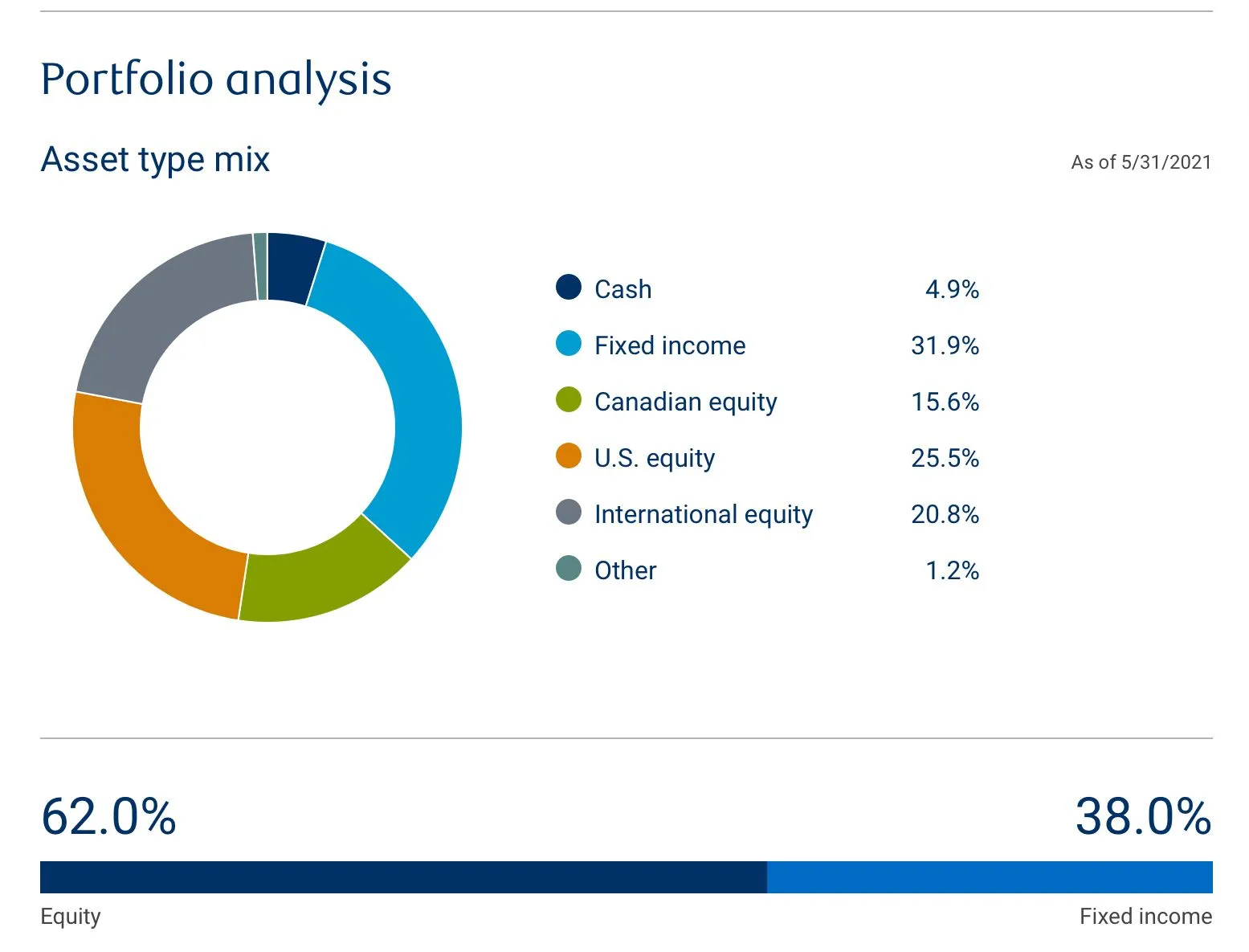

Let’s say this RBC balanced mutual fund is yours. Looking at the pie chart they provide:

~32% fixed income, 25% US equities, 15% CA equities, and 20% international (international may also include “emerging markets”), 5% cash, 2% other.

If we look at the index funds listed here and start with the balanced funds we can also look up their prospectus and compare.

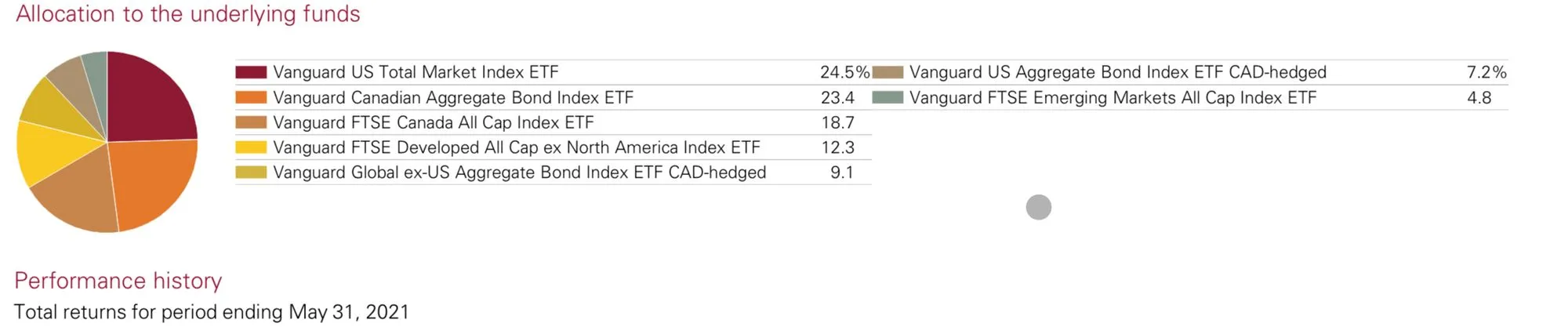

VBAL

VBAL is Vanguard’s balanced index portfolio, basically seven Vanguard index funds balanced for your specific risk, with an MER of 0.25%.

This might look more complex but it’s pretty similar to RBC:

~39% bonds (23% + 9% + 7%), 25% US equities, 19% CA equities, 12% international, 5% emerging markets. The fee for VBAL is 0.25% vs 1.97% for RBC.

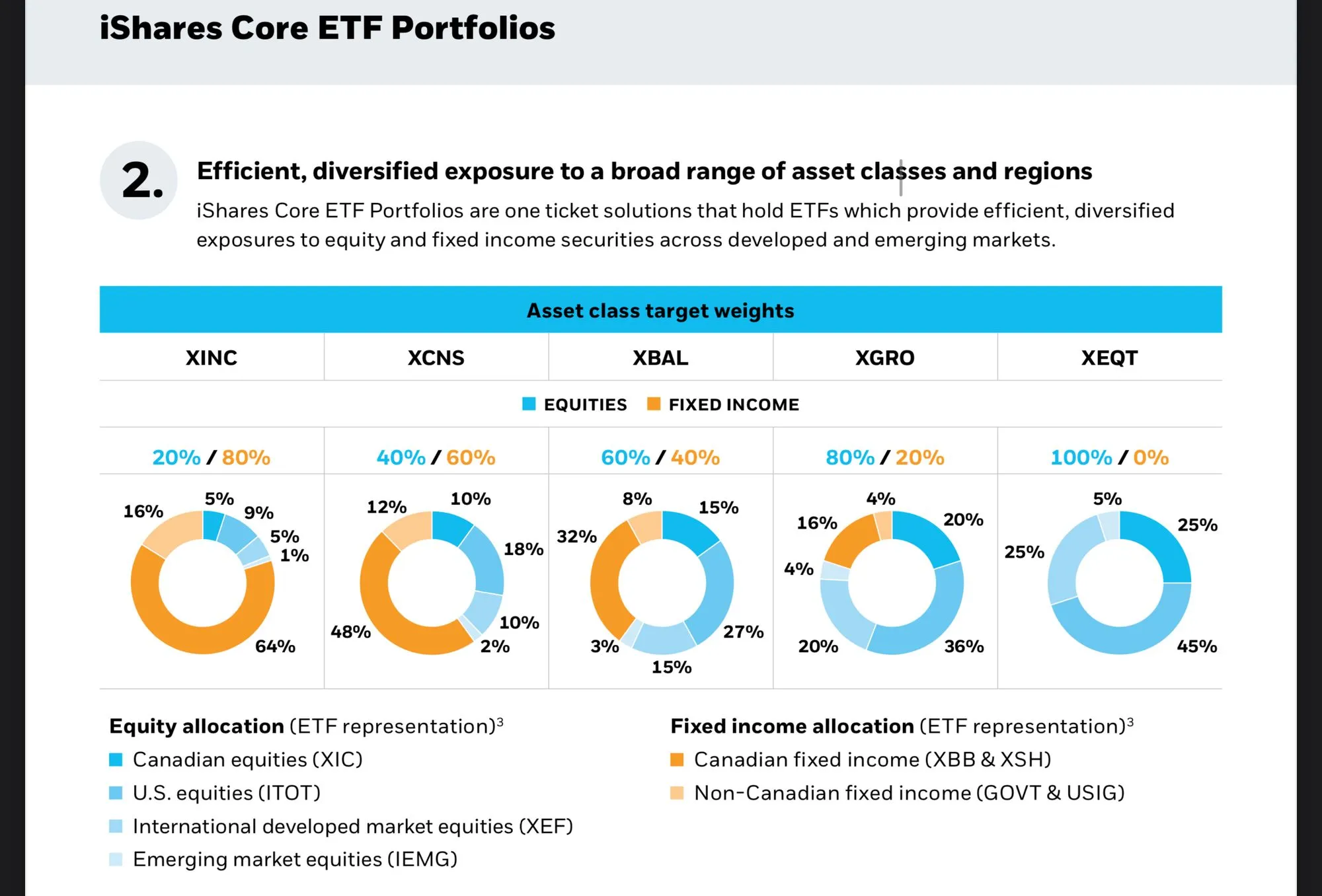

XBAL

XBAL sits in the middle of the above chart. BlackRock is the company behind many “iShares” index funds (usually with an “X” at the beginning), and they’re usually a little cheaper than Vanguard’s index funds. XBAL is composed of eight other iShares indexes. Again this is very similar to RBC’s spread and comes in with a 0.2% fee.

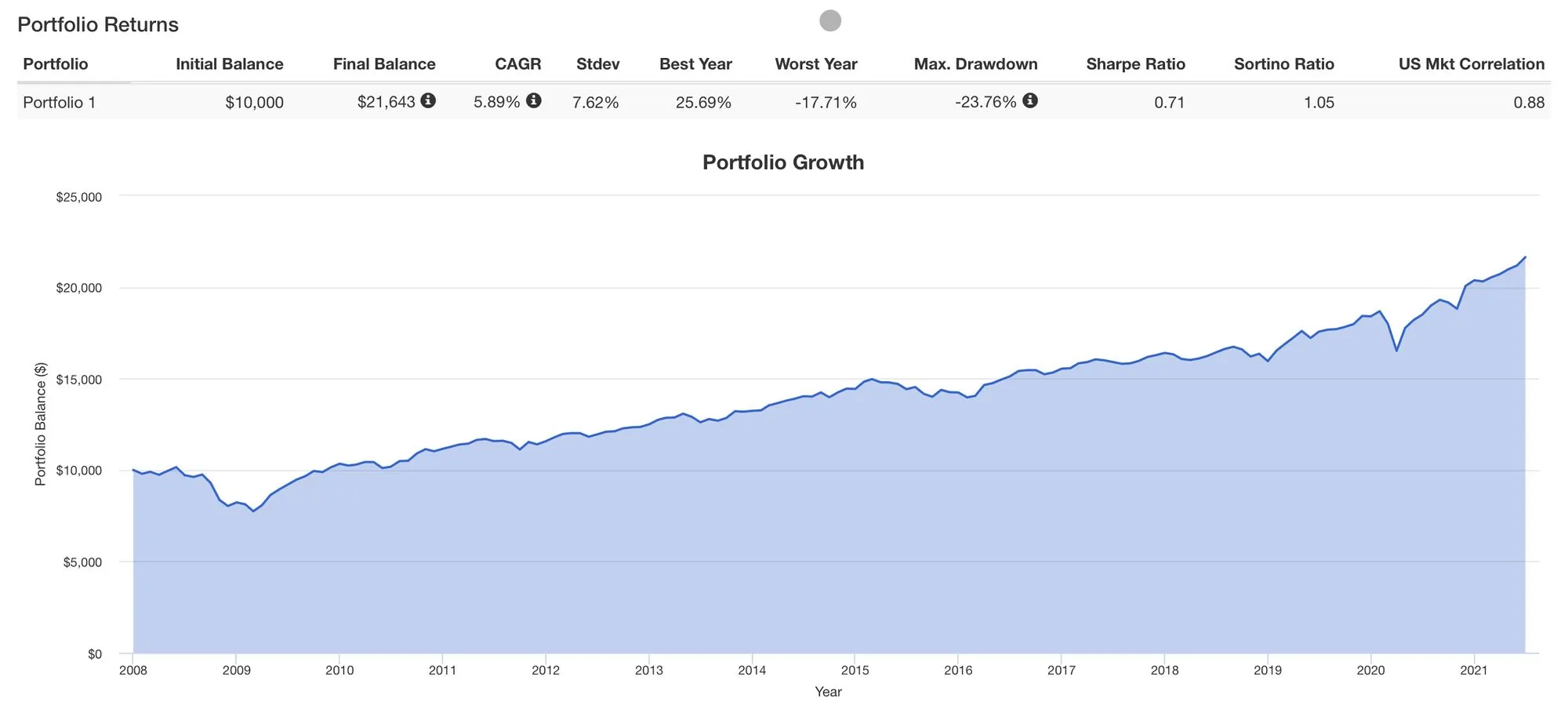

Now what about the returns?

I know I said not to look at the returns, but just to prove the point that it really doesn’t matter what index you pick, here is a backtest:

We can look specifically at XBAL which has been around for a lot longer:

I even compared this to the RBC mutual fund and the 5-year average return with RBC was 5.2% (after 2% fee); XBAL was 7.4%. When you factor in the fee they look similar for headline returns, but after fees RBC underperforms by thousands of dollars, hundreds of thousands in the long run.

Next steps

If you want to avoid paying these high fees for little value, follow the steps in Self-directed investing in 5 steps. After you’re set up, Reduce fees on index funds covers buying the underlying ETFs to cut MER further if you want to optimize.

I have had friends set up and initiate their TFSA transfer in as little as an hour and set up a portfolio on Passiv. You can use this model I made if you want.

Honestly I think you could set up your Questrade/Passiv account in under an hour given you’ll be setting up a one-fund portfolio. The longest part will be waiting for the TFSA to transfer from your bank.

Notes about fees and alternatives

Questrade has no fees for purchasing most index funds or ETFs, but sometimes there is a 1-cent fee per unit capped at $5 per transaction, negligible compared to most other services.

Wealthsimple Trade also allows you to buy index funds for free, but I hesitate to recommend them as their business model seems more aligned with promoting stock picking and active trading rather than passive investing.